Sarah runs an online store selling home décor products. At the end of the year, she checks her business bank account, $180,000 sitting there. She assumes it was a great year.

Then her accountant sends over the profit and loss statement.

Net income: $11,000.

She stares at the screen for a long time.

Where did the rest go? How can she have moved $600,000 worth of products and only kept $11,000? And what does that $180,000 in the bank actually mean if it is not her profit?

This is the confusion that trips up thousands of small business owners every year. Revenue feels like success. Cash in the account feels like profit. But neither of those numbers tells you whether your business is actually making money.

It is the single most important number on your financial statements. It tells you what is left after every dollar has been earned and every expense has been paid. It is the number lenders look at, the number that determines your tax liability, and the number that, when tracked properly tells you whether your business is growing, shrinking, or just spinning its wheels.

This guide will show you exactly what net income is, how to calculate it step by step, how to analyze it so it actually means something, and how to avoid the mistakes that make the number misleading.

What Net Income Actually Is

Net income is the amount of money your business keeps after paying for everything it costs to operate.

Not revenue. Not gross profit. Not what came into your account. What actually remains after every single expense, cost of goods, rent, salaries, software, interest on loans, and taxes has been deducted.

Here is the simplest way to think about it:

Every dollar your business earns goes somewhere. Net income is whatever is left over after it all goes where it needs to go.

Because it sits at the very bottom of the profit and loss statement after every line of income and every line of expense it is called the bottom line. When someone says “what is your bottom line,” they are asking about net income.

You will also hear it called:

- Net profit

- Net earnings

- After-tax income

- The bottom line

All the same number. All meaning the same thing: what your business actually made.

Why Revenue Alone Tells You Nothing

This is the most important mindset shift for any small business owner.

Revenue or total sales tells you how much came in. It says nothing about what it cost to generate that sales figure, what you paid to run the business, or what you owe in taxes.

A business doing $2 million in revenue can have a net income of $40,000. Another business doing $400,000 in revenue can have a net income of $120,000.

The second business is three times more profitable despite being five times smaller in revenue.

Net income is the number that actually measures success.

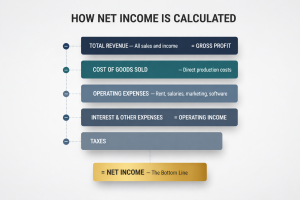

The Net Income Formula

The Simple Version

This is the foundation. Everything you earned, minus everything you spent.

The Full Version

This expanded version breaks down exactly where the money goes at each stage. Here is what each component means:

| Component | What It Means |

| Revenue | All income from sales of products or services |

| COGS (Cost of Goods Sold) | Direct costs of producing what you sell inventory, materials, manufacturing |

| Operating Expenses | The cost of running the business rent, salaries, marketing, software, utilities |

| Interest | Cost of any debt business loans, lines of credit |

| Taxes | Federal, state, and local income taxes owed |

Single-Step vs Multi-Step Calculation

Single-step simply totals all revenue and subtracts all expenses in one calculation. Clean and fast useful for very small businesses or internal reporting.

Multi-step works through the calculation in stages gross profit first, then operating income, then pre-tax income, then net income. This gives you far more visibility into where profit is being made and lost, and is the standard format for most business financial statements.

For any business beyond the very earliest stage, the multi-step approach is worth the extra work. You will see exactly why in the next section.

Step-by-Step Calculation With a Real Example

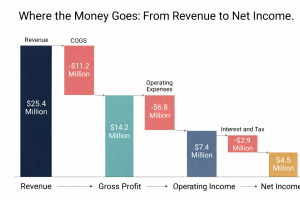

Let us walk through a full example using Hartwell Home Co. a small e-commerce business selling premium candles and home fragrance products online.

Here is their annual financial data:

- Total Revenue (Sales): $620,000

- Returns and Refunds: $18,000

- Net Revenue: $602,000

- Cost of Goods Sold: $241,000 (wax, fragrance, jars, packaging, labels)

- Operating Expenses: $228,000 (warehouse rent, salaries, marketing, platform fees, software, shipping supplies)

- Interest on Business Loan: $9,500

- Income Taxes: $18,200

Step 1: Calculate Net Revenue

$$$620,000 – $18,000 = $602,000$$

Always start with actual net revenue gross sales minus returns. This is your real starting point.

Step 2: Calculate Gross Profit

$$$602,000 – $241,000 = $361,000$$

Hartwell Home Co. keeps $361,000 after paying for the products themselves. This looks strong. But the story is not over.

Step 3: Calculate Operating Income

$$$361,000 – $228,000 = $133,000$$

After paying to run the business the warehouse, the staff, the ads, the Shopify subscription, the email platform operating income is $133,000.

Step 4: Calculate Pre-Tax Income

$$$133,000 – $9,500 = $123,500$$

Step 5: Calculate Net Income

$$$123,500 – $18,200 = $105,300$$

Hartwell Home Co.’s net income: $105,300.

Out of $620,000 in gross sales, the business keeps $105,300. That is a net profit margin of approximately 17.5% a healthy result for an e-commerce business.

What If the Numbers Go the Other Way?

Now imagine Hartwell had a harder year. They ran a warehouse sale, refunds were higher, and they hired an extra team member mid-year.

- Net Revenue: $480,000

- COGS: $221,000

- Operating Expenses: $274,000

- Interest: $9,500

- Taxes: $0 (no profit, no tax)

Net income: -$24,500. A net loss.

This is not a failure that signals the business should close but it is a clear signal that operating expenses outpaced gross profit, and something needs to change. Net income makes that visible. Revenue alone would not.

Net Income vs Gross Profit vs Operating Income

These three numbers live on the same profit and loss statement but tell completely different stories. Confusing them is one of the most common mistakes small business owners make.

| Metric | What It Measures | Formula |

| Gross Profit | Profitability of your product before operating costs | Revenue − COGS |

| Operating Income | Profitability of your core business operations | Gross Profit − Operating Expenses |

| Net Income | Total profitability after everything | Operating Income − Interest − Taxes |

Why This Matters in Practice

A business can have strong gross profit and weak net income. This means the product itself is profitable, but operating costs, staff, marketing, rent, software are eating the margin.

A business can have strong operating income but lower net income. This means the operations are efficient, but heavy debt (interest) or a large tax bill is pulling the final number down.

Gross profit tells you if your product pricing and production costs are working. Operating income tells you if your business model is efficient. Net income tells you if the whole thing product, operations, debt, and taxes is actually working.

For Hartwell Home Co., gross profit was a healthy $361,000, but operating expenses took the majority of that. Net income of $105,300 is good but the gap between gross profit and net income signals that operating expenses deserve close attention as the business scales.

Net Income vs Cash Flow, The Confusion That Costs Businesses

This is the section most financial guides skip over or explain badly. It is also the confusion that causes the most real-world damage to small business owners.

Net income and cash in your bank account are not the same thing.

Sarah, the business owner from the introduction is not an unusual case. It is entirely possible, and extremely common, for a business to show strong net income on paper while the owner is stressed about making payroll. It is also common to have cash in the account that feels like profit but is not.

Here is why.

Accrual Accounting vs Cash Basis

Most businesses using proper accounting software operate on accrual accounting. This means:

- Revenue is recorded when it is earned not when the cash arrives

- Expenses are recorded when they are incurred not when you pay the bill

So if Hartwell Home Co. sells $40,000 worth of products in December but the payment processor does not transfer the funds until January that $40,000 is counted as December revenue and included in net income for that year, even though the cash has not arrived yet.

Similarly, if they receive $15,000 in inventory in December on net-30 payment terms that cost hits December’s expenses even though the cash does not leave their account until January.

Under cash basis accounting, revenue and expenses are only recorded when cash actually moves. This is simpler but gives a less accurate picture of true business performance.

Three Ways Net Income and Cash Flow Diverge

- Accounts Receivable You invoice a wholesale customer for $25,000. They pay 60 days later. The $25,000 is net income now. The cash arrives later.

- Inventory Purchases You spend $80,000 on inventory in Q4 to prepare for the holiday season. That cash is gone. But it only hits net income as COGS when the products are actually sold not when you bought the stock.

- Loan Repayments You make $3,000 monthly payments on a business loan. Only the interest portion of that payment reduces net income. The principal repayment is not an expense it reduces your liability on the balance sheet. So $36,000 in annual loan payments might only reduce net income by $9,500 in interest, while the other $26,500 in principal repayments drains cash with no income statement impact.

The Critical Point

A business can be profitable on paper and still run out of cash. And a business can have cash sitting in the account that is not profit it might be unspent loan proceeds, deposits from customers not yet fulfilled, or simply timing differences.

This is why professional bookkeepers track both net income and cash flow and why you should never use your bank balance as a substitute for reading your P&L.

How to Analyze Net Income: What the Number Actually Tells You

Calculating net income is the start. Analyzing it is where the real value is.

A standalone net income figure $105,300 means very little without context. Here is how to turn that number into useful business intelligence.

Net Profit Margin

Net Profit Margin = Net Income / Revenue ×100

For Hartwell Home Co.:

Net Profit Margin= 105,300 / 602,000

This means for every dollar of revenue, the business keeps $0.175 as profit.

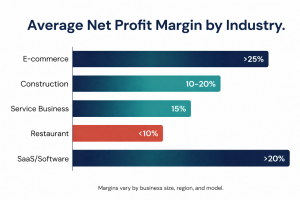

What is a good net profit margin? It depends heavily on the industry:

| Industry | Typical Net Profit Margin |

| E-commerce (retail) | 5% – 20% |

| Construction | 2% – 8% |

| Service businesses | 15% – 30% |

| Restaurants | 3% – 9% |

| SaaS / Software | 20% – 40% |

Hartwell’s 17.5% sits at the strong end for e-commerce. But if it drops to 8% next year with the same revenue, that is a signal worth investigating immediately.

Year-Over-Year Trend Analysis

A single year of net income tells you one data point. Two or three years tells you a story.

If revenue grows 20% but net income grows only 5%, operating expenses are growing faster than the business can profitably scale. That is a warning sign hidden inside what looks like good revenue growth.

If revenue stays flat but net income grows, the business is getting more efficient a very good sign.

Always compare net income as both a dollar figure and a percentage of revenue. The percentage reveals margin compression or improvement that the raw number can hide.

When Net Income Is Misleading

Net income can be distorted in ways that make a business look more or less profitable than it actually is:

- One-time events: A business sells a piece of equipment for a gain. Net income spikes. Operating performance has not improved.

- Depreciation timing: Large assets depreciate over time. Depending on the depreciation method used, net income can shift significantly year to year.

- Owner compensation: In a sole proprietorship or single-member LLC, if the owner does not pay themselves a formal salary, operating expenses look lower and net income looks higher. It is not a real reflection of profitability.

When net income looks unusually high or low, dig into the details before drawing conclusions.

Where Net Income Appears Across Financial Statements

Net income does not live in isolation. It connects all three of your core financial statements — and understanding those connections gives you a much clearer picture of your business health.

The Income Statement (Primary Home)

This is where net income is calculated and reported. Every line of revenue and every line of expense leads to the final net income figure at the bottom. If you only read one financial statement, this is the one.

The Balance Sheet Retained Earnings

At the end of the period, net income flows into the retained earnings section of the balance sheet. Retained earnings represent the cumulative profit the business has kept over time rather than distributing to owners.

If Hartwell Home Co. had $60,000 in retained earnings at the start of the year and earned $105,300 in net income and the owner did not take any distributions retained earnings at year end would be $165,300.

This is how a profitable business builds equity over time.

The Cash Flow Statement Operating Activities

The cash flow statement starts with net income and then adjusts it for non-cash items and working capital changes to arrive at actual cash generated from operations.

This is why the cash flow statement begins with net income and then makes all the adjustments (like changes in accounts receivable, inventory, and depreciation) that explain the gap between profit on paper and cash in the bank.

Understanding this link answers the question Sarah was asking at the start: how do I have $180,000 in the bank if my net income is only $11,000? The cash flow statement reconciles exactly that.

Common Mistakes That Distort Net Income

Knowing the formula is one thing. Getting an accurate number is another. These are the most common errors that make net income misleading:

1. Mixing Personal and Business Expenses

Running personal expenses groceries, holidays, personal subscriptions through the business reduces net income artificially and creates tax and legal problems. Keep accounts completely separate.

2. Missing Depreciation Entries

If you buy a $15,000 piece of equipment and expense the entire amount in year one, net income takes an artificial hit. Depreciation spreads the cost over the asset’s useful life. Missing or incorrectly recording depreciation distorts net income for multiple years.

3. Incorrectly Categorizing COGS vs Operating Expenses

This changes where profit appears on the P&L. Miscategorizing direct product costs as operating expenses or vice versa makes gross profit and operating income both misleading, even if net income ends up in the same place.

4. Not Accounting for Owner’s Salary

This is especially common in sole proprietorships and single-member LLCs. If you are running the business and not paying yourself a formal salary, your operating expenses are understated. Net income looks higher than it really is because your labor cost is invisible. When analyzing true profitability, always factor in what you would pay someone else to do your job.

5. Forgetting Quarterly Estimated Taxes

If you operate as a self-employed individual or pass-through entity, income taxes may not appear as a deduction in your bookkeeping during the year. Forgetting to account for the tax liability means net income looks higher than the amount you will actually keep.

Frequently Asked Questions

Q: What is the net income formula for self-employed individuals? For self-employed individuals, net income is calculated the same way: Total Revenue minus Total Business Expenses. However, you also need to subtract the self-employment tax deduction (50% of self-employment taxes paid) before arriving at your net self-employment income for tax purposes.

Q: What is the difference between net income and taxable income? Net income is your accounting profit calculated according to accounting principles on your P&L. Taxable income is calculated according to tax rules, which differ in how they treat certain deductions, depreciation, and credits. The two numbers are often different, which is why your accountant makes adjustments when preparing your tax return.

Q: Can net income be negative? Yes. A negative net income is called a net loss. It means total expenses exceeded total revenue for the period. A net loss in one period is not automatically a crisis many businesses run a loss during growth phases or difficult market conditions but persistent net losses indicate the business model needs adjustment.

Q: Where do I find net income on a tax return? For sole proprietors, net income appears on Schedule C of your personal tax return as net profit or loss. For S corporations, it appears on Form 1120-S. For C corporations, it is on Form 1120. The specific line varies by form, but it is always the bottom-line profit or loss figure.

Q: How often should I calculate net income? At minimum, monthly. Waiting until year-end to review net income means spending twelve months making decisions without knowing whether the business is profitable. Monthly P&L reviews let you catch problems early a rising expense category, a shrinking margin before they become serious.

Q: What is the difference between net income and EBITDA? EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. It is net income with those four items added back. EBITDA is used to evaluate a business’s core operational profitability independent of financing decisions and accounting methods. It is commonly used in business valuations and by investors, but it is not a substitute for net income in day-to-day financial management.

Final Thought

Net income is not just an accounting figure you hand to your accountant once a year. It is the most direct measurement of whether your business is building something or slowly draining it.

Understanding how it is calculated shows you where the money goes. Understanding how to analyze it tells you what to do next. And understanding how it connects to cash flow, retained earnings, and your tax return gives you the complete financial picture that most small business owners never get because nobody sat down and explained it clearly.

Now you have that picture.

If your net income numbers are raising questions, or if you are not confident the figures in your books are accurate, that is exactly the kind of problem a professional bookkeeper can help you solve before it costs you more than a conversation.